A Founder’s Guide to Financial Due Diligence Preparation

Insight

Subscribe to our

Newsletter

Newsletter

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Due diligence is one of the most consequential stages of a fundraising process. It directly influences valuation adjustments, deal timelines, and investor confidence.

Let’s start with financial due diligence (FDD), which is usually the most comprehensive among the typical diligence tracks, as it tests both performance and internal controls. It’s often misunderstood, and founders sometimes approach it as an exercise in presenting perfect numbers. Investors, however, are assessing reliability, consistency, and risk exposure. The gap between these two expectations is where most FDD processes fail.

Financial due diligence is not an audit. It is a structured way for investors to answer a few simple questions:

- Do we understand how this business makes money?

- Do the numbers reconcile across systems and time?

- Are there hidden risks that could affect valuation?

In practice, investors typically move through a data room sequentially, starting with financial statements and then drilling into revenue, cost drivers, and finally ownership and contingencies. Preparation should mirror that sequence.

This article outlines a practical FDD preparation structure, based on how investors typically review a data room.

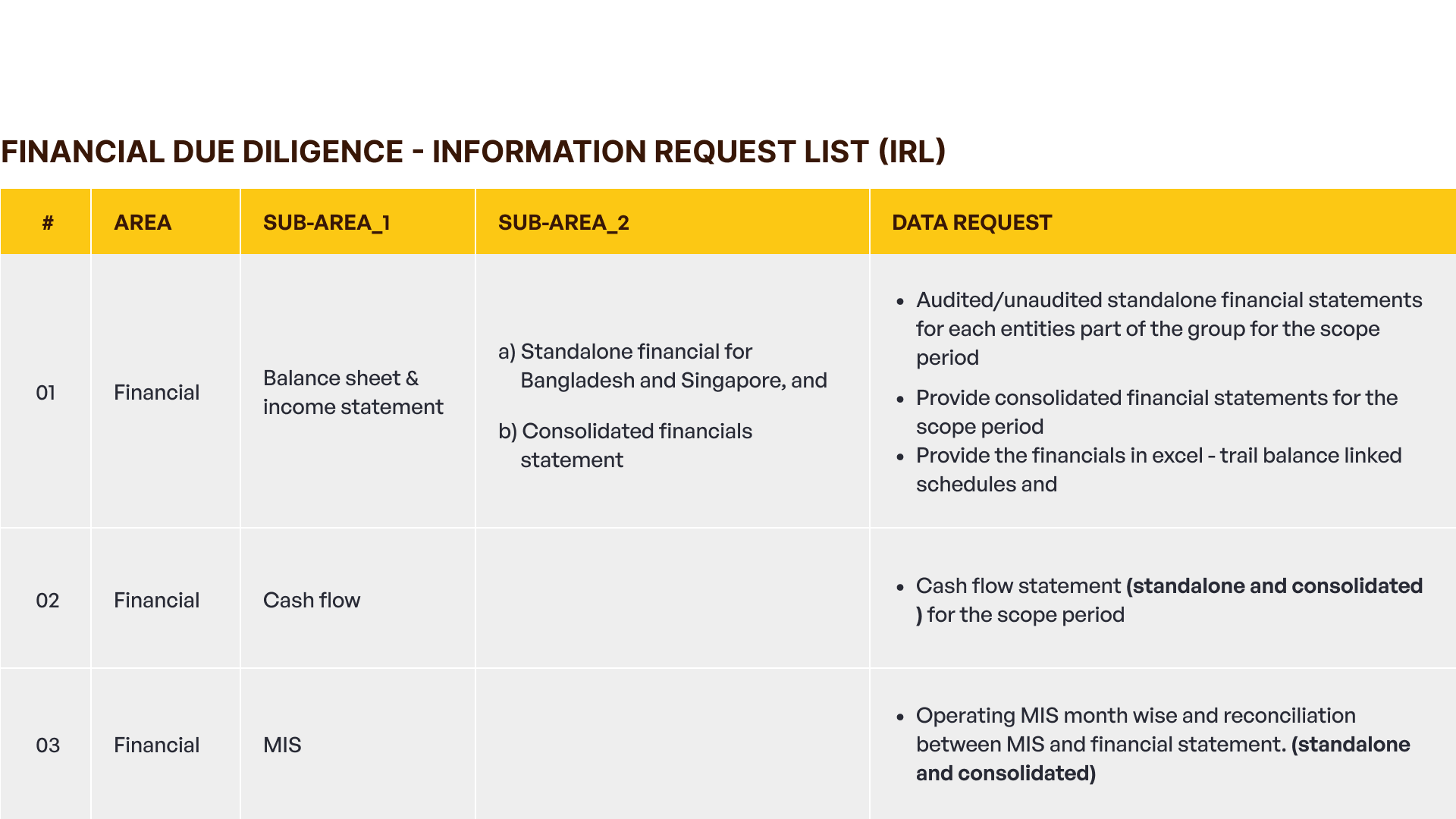

Segment 1: Core Financial Statements and MIS

This is where FDD begins. Before investors assess growth or projections, they need to understand the financial foundation.

What this segment is really about:

- The income statement shows how the business performed

- The balance sheet shows where the business stands

- The cash flow statement shows how money actually moved

- The MIS shows how you manage the business

Founders often encounter and worry about gaps between MIS and financial statements. This is a common issue. What matters is whether you can explain those gaps clearly.

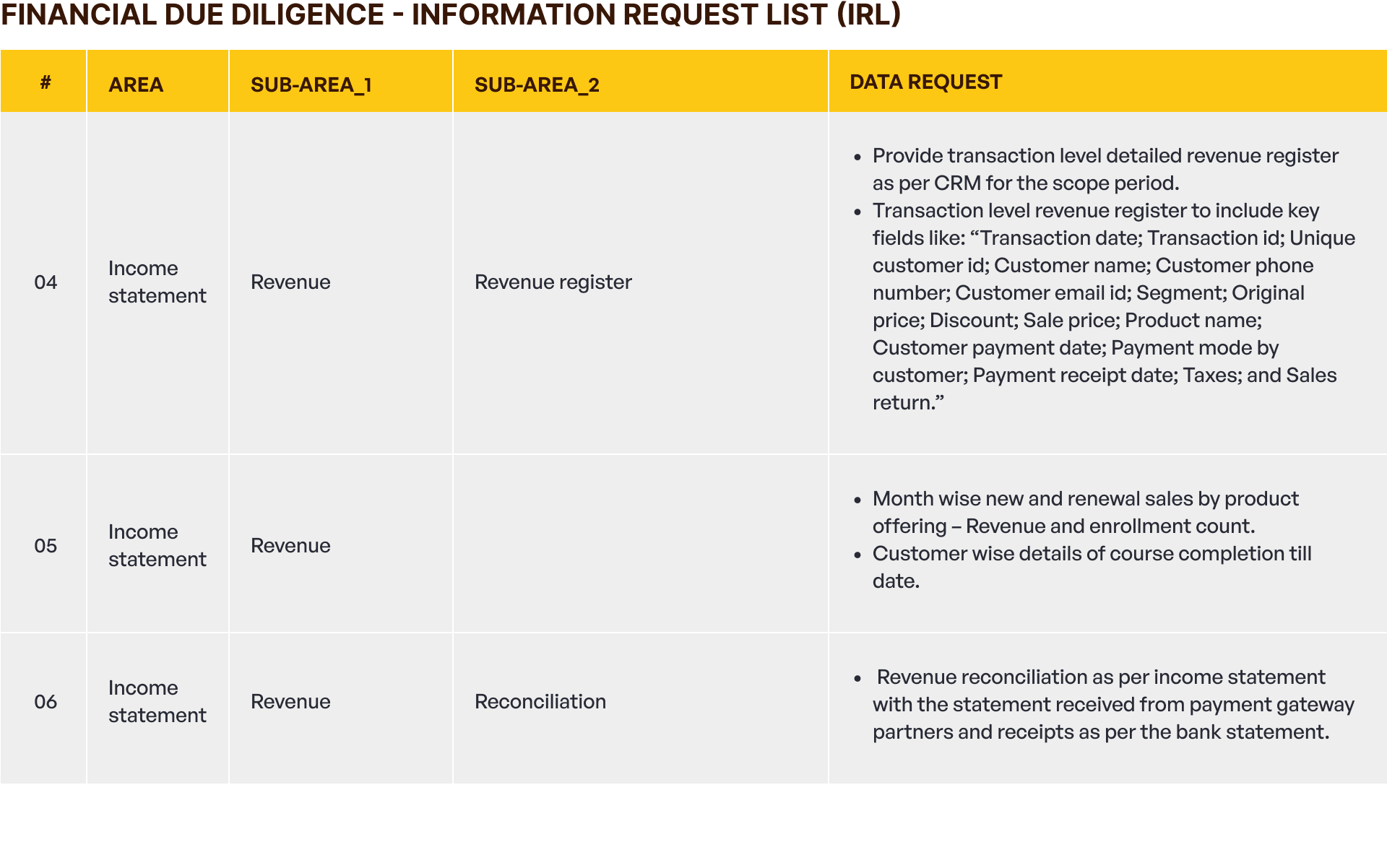

Segment 2: Revenue Detail and Reconciliation

While investors review summaries, validation actually happens at the transaction level.

This segment shows:

- That reported revenue can be traced back to real customers

- That pricing, discounts, refunds, and taxes are properly captured

- That revenue recorded eventually turns into cash

Clean reconciliation between CRM, payment gateways, and bank statements builds credibility. Poor reconciliation leads to multiple follow-ups and delays fundraising.

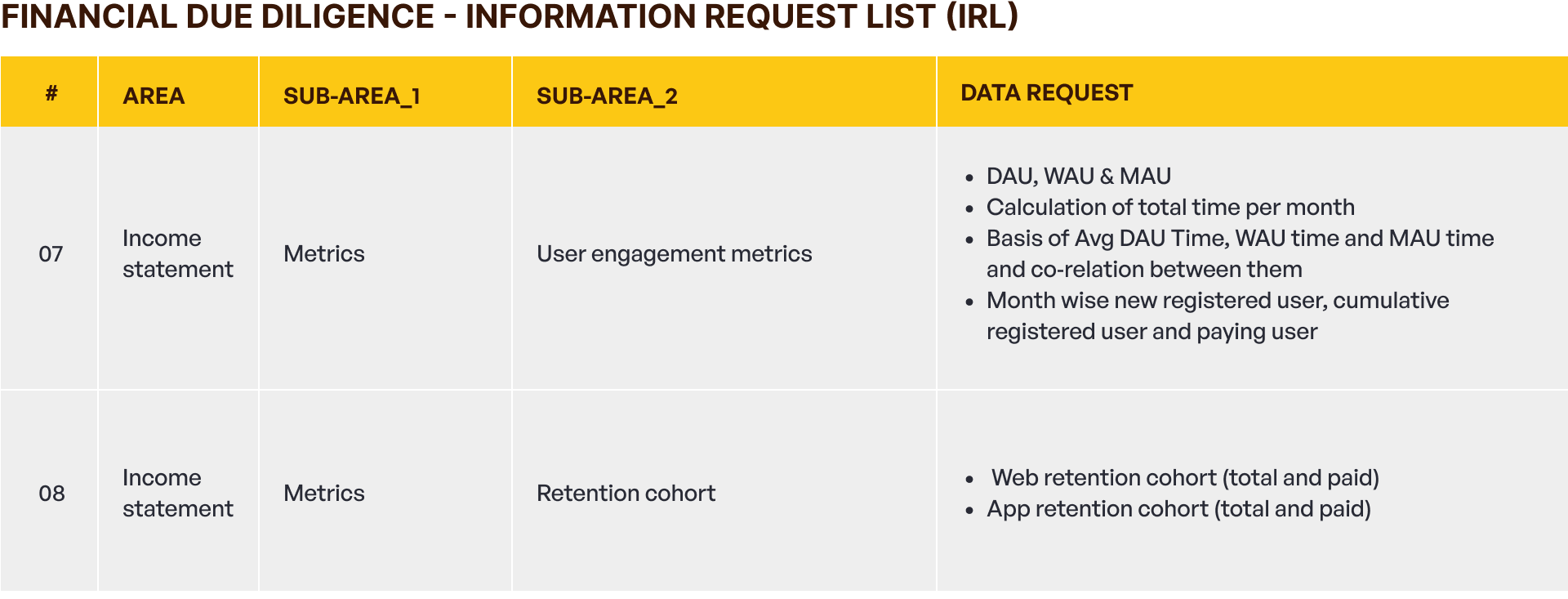

Segment 3: User Metrics and Retention

For digital and product-led startups, revenue alone is not enough. Investors want to know whether user behavior supports it.

Investors assess:

- Engagement metrics, which explain how often users return

- Conversion metrics, which explain how users become paying customers

- Retention cohorts, which explain how long the value lasts

Founders sometimes treat metrics as storytelling tools. In FDD, they are validation tools. Weak retention does not automatically derail a deal. Unexplained or inconsistent retention data, however, introduces uncertainty into revenue sustainability assumptions.

Segment 4: Cost of Goods Sold and Gross Margin

After validating revenue, investors ask a simple question: What does it cost to deliver this? This segment tests whether gross margins are appropriately calculated.

Review areas include:

- Identification of all costs directly tied to revenue

- Ensuring relevant costs are captured correctly

- Understanding the proper gross margin level levers.

If margins appear unusually strong relative to comparable companies, this section receives deeper scrutiny, and investors may challenge cost classification decisions.

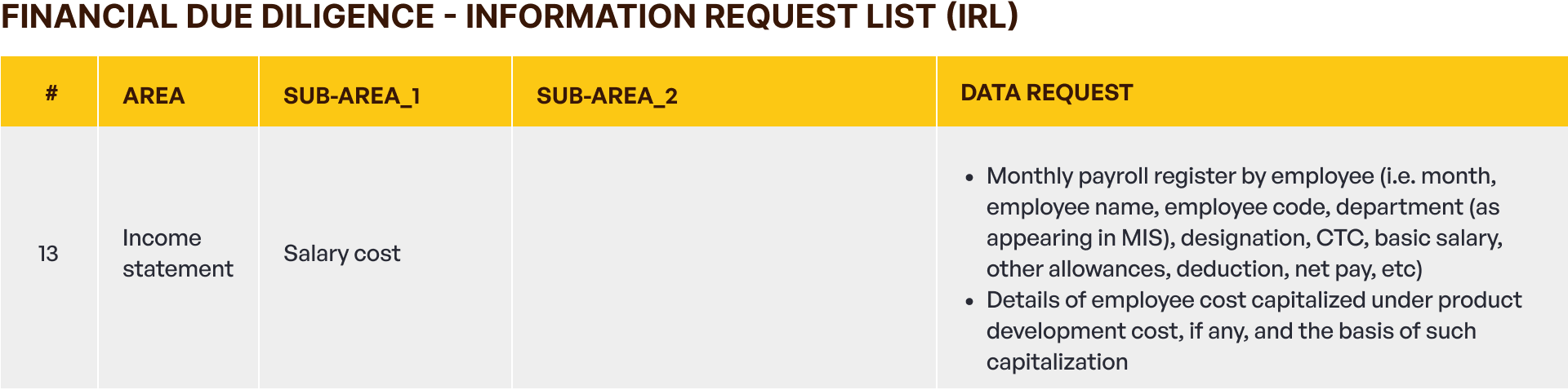

Segment 5: Salary Costs and Payroll

Payroll is usually the highest fixed cost and the hardest to adjust quickly.

What this segment is really about:

- Showing how the team is structured

- Demonstrating cost discipline relative to the stage and competitors

- Explaining any capitalization of employee costs

Founders should expect detailed questions here and have proper justification ready.

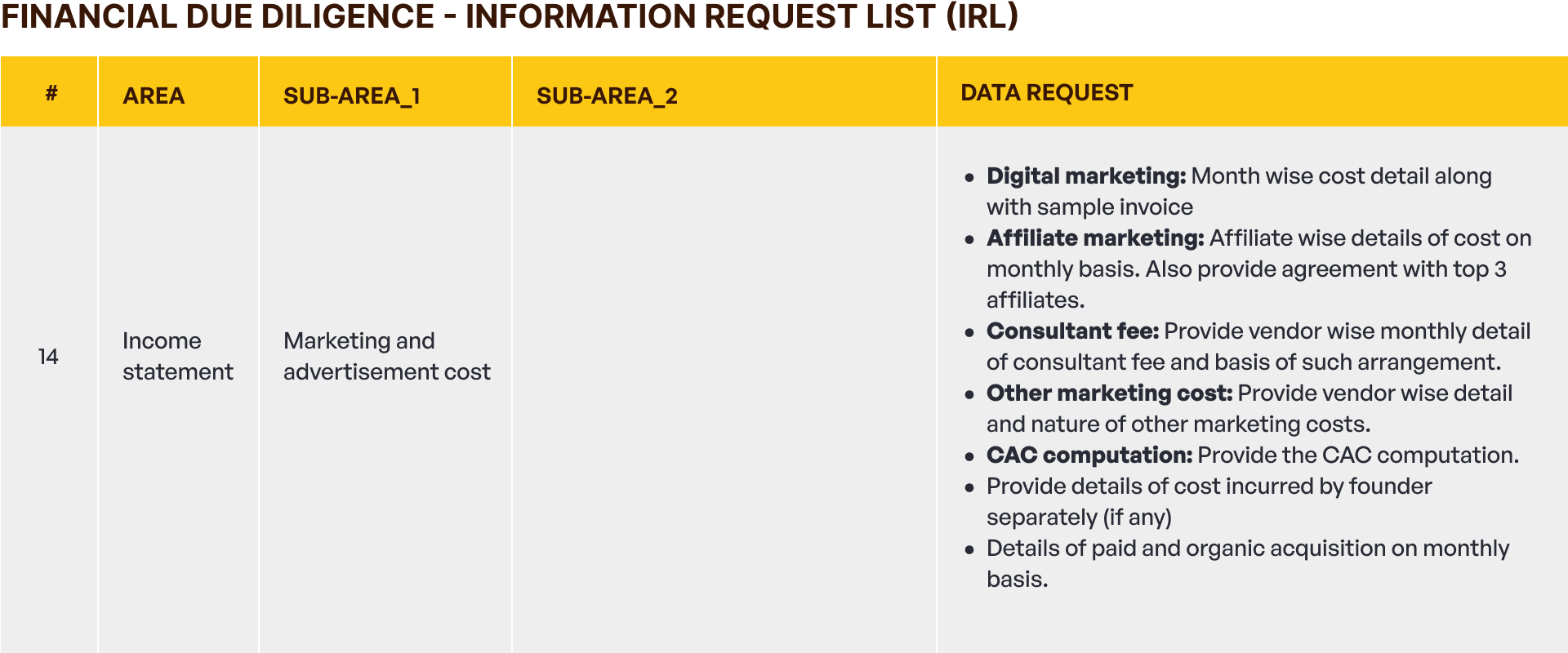

Segment 6: Marketing Spend and CAC

This is where investors evaluate whether growth is efficient and sustainable.

Investors analyze:

- Marketing spend by channel, and whether it leads to user acquisition

- Customer acquisition cost (CAC) calculation methodology

- Dependency on paid channels versus organic acquisition

CAC levels do not need to be minimal, nor does growth need to be aggressive. What investors require is clarity on unit economics and scalability assumptions.

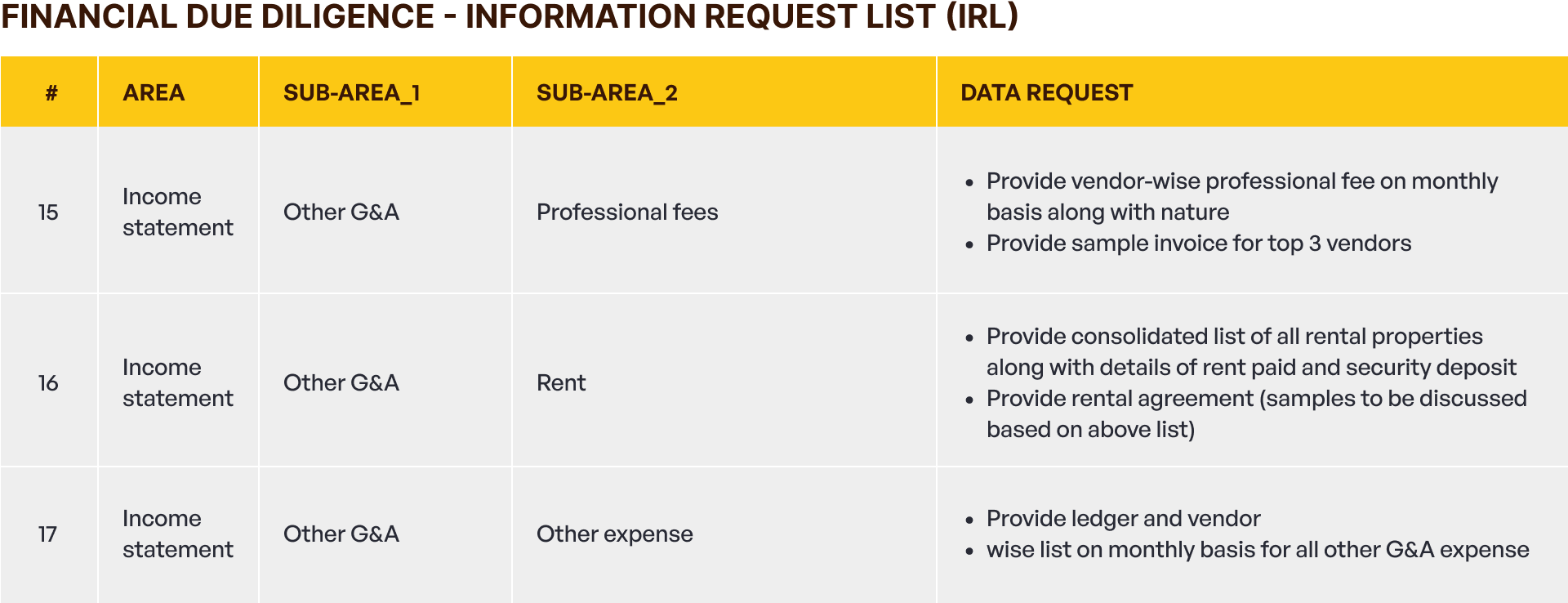

Segment 7: G&A and Overhead Costs

General and administrative costs reveal how the company operates behind the scenes.

This segment focuses on:

- Understanding baseline operating costs

- Identifying long-term commitments

- Testing cost classification discipline

Investors assess whether overhead growth is proportional to company scale and whether fixed cost structure introduces downside risk. This section often highlights structural inefficiencies that may not be visible in topline metrics.

Segment 8: Assets and Capitalization

This is where accounting decisions directly affect reported performance.

Investors want to know:

- Whether assets recorded on the balance sheet are defensible

- How development costs are capitalized

- Whether amortization and depreciation are applied consistently

Investors expect sound judgment here. They do not expect aggressive capitalization.

Segment 9: Working Capital and Liquidity

his demonstrates whether the business is financially stable day to day.

Key areas include:

- Accounts receivable aging and collection cycles

- Accounts payable timing and vendor relationships

- Cash balances and restrictions

Liquidity pressures typically surface here before appearing anywhere else.

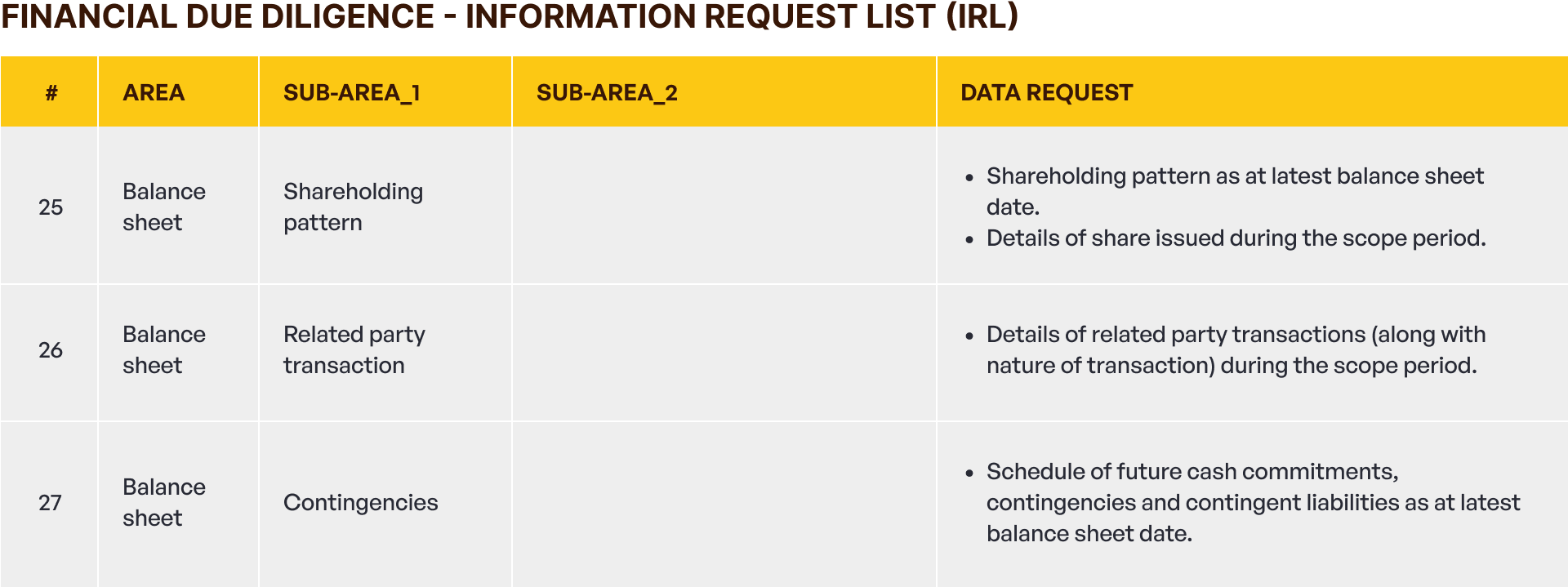

Segment 10: Ownership, Related Parties, and Contingencies

This final layer often carries a significant impact on the deal.

Investors review:

- Ownership clarity and equity history

- Transparency around related party dealings

- Future obligations and contingent risks

Undisclosed related party transactions or equity inconsistencies can materially delay deal closing, even if financial performance is strong.

Financial due diligence is not about perfection. It is about coherence, traceability, and risk transparency. Founders who can reconcile performance across financial statements, operational dashboards, and bank records reduce diligence friction and strengthen negotiation position.

Related Articles

View All

.jpg)

.jpg)

.png)

.jpg)

.jpg)

.jpeg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpeg)