What Investors Actually Check in Tax Due Diligence

Insight

Subscribe to our

Newsletter

Newsletter

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Shoumik Shahriar is a Senior Business Consultant and Project Manager at LightCastle Partners, a management consulting firm based in Bangladesh.

Due diligence is one of the most consequential stages of a fundraising process. It shapes valuation, deal timelines, and investor confidence. This is the second part of a three-part series on preparing for it. Part one covered financial due diligence; this part turns to tax.

In tax due diligence (TDD), investors are testing whether a company’s tax position is consistent, reconciled, and free of undisclosed exposure. It comes down to three questions:

- Are all statutory tax obligations properly complied with?

- Do tax numbers reconcile with the financial statements?

- Are there any past or ongoing tax risks that could affect valuation?

This article walks through a practical TDD preparation structure, based on how investors actually review tax documentation in a data room. Each segment below pairs the documentation investors request with a short explanation of what they are checking and why.

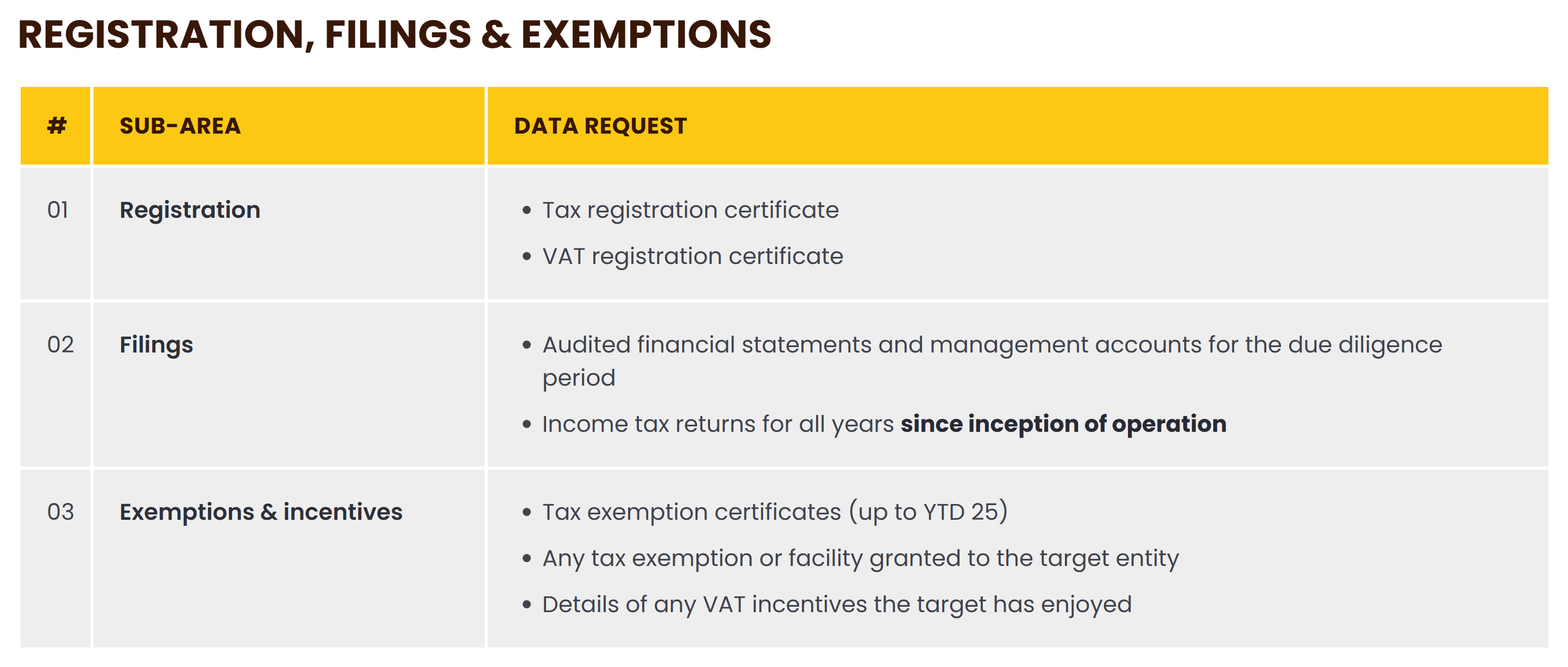

Segment 1: Registration, Filings & Exemptions

Tax diligence starts with basic legitimacy. Investors first verify whether the company is properly registered with the relevant tax authorities and whether statutory filings have been made consistently. This includes reviewing tax registration certificates, VAT registration certificates, audited financial statements, management accounts, and income tax returns filed since inception. If the company has enjoyed any tax exemptions, incentives, or special facilities, the approval letters and supporting documentation are examined closely.

This segment establishes whether the company has a clean compliance foundation. Missing filings or expired registrations immediately slow down the process and raise concerns about broader discipline.

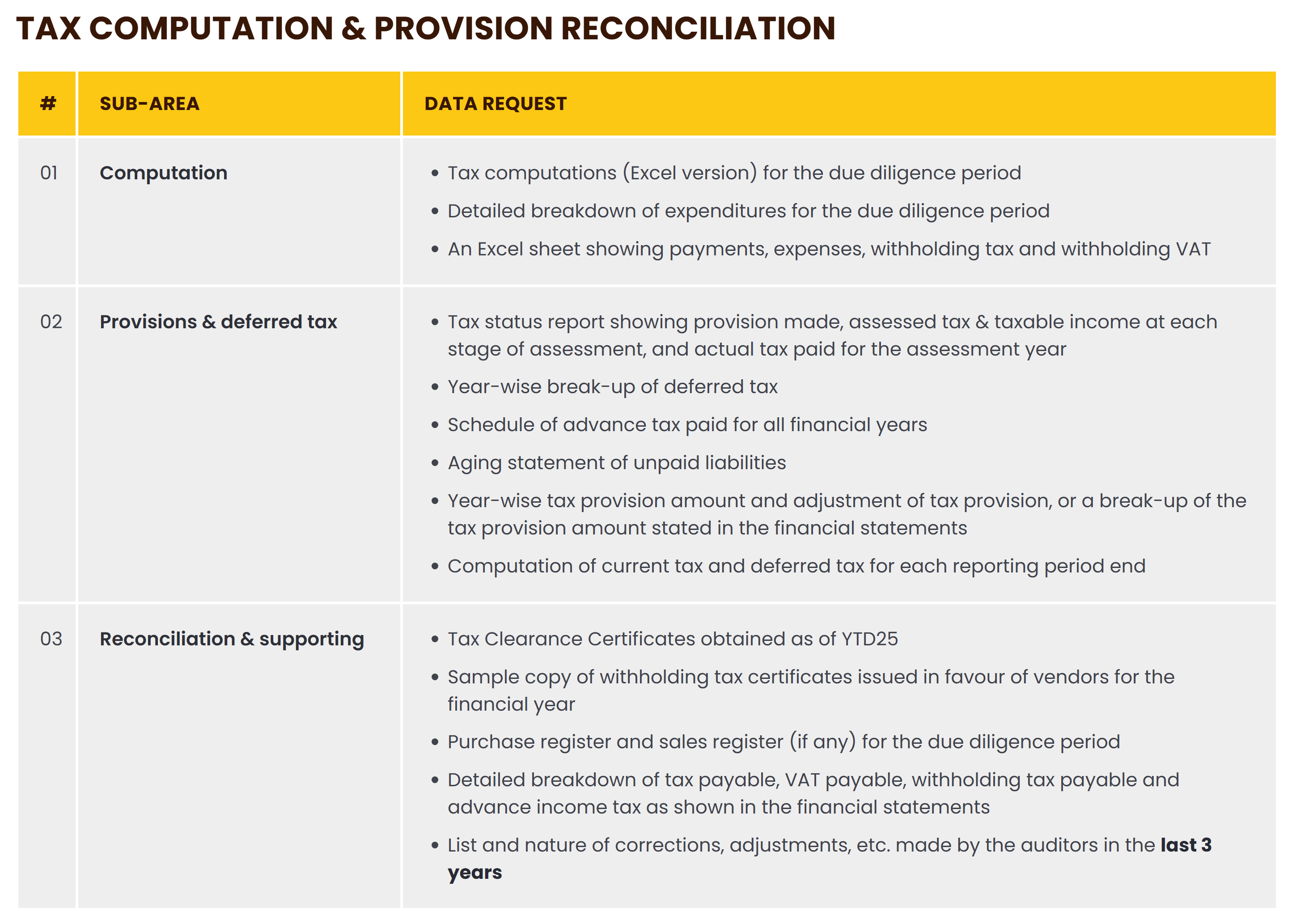

Segment 2: Tax Computation & Provision Reconciliation

Once filings are confirmed, attention shifts to numbers. Investors review detailed tax computation files, expenditure breakdowns, tax status reports showing assessed income and tax paid, deferred tax movements, advance tax schedules, and aging of unpaid tax liabilities. They also look at withholding tax reconciliations, purchase and sales registers, breakdowns of tax payable balances, auditor adjustments affecting tax, and current-versus-deferred tax calculations as of reporting dates.

This segment focuses on consistency across records. Differences between management account figures and statutory calculations are common, but the linkage between them should be clear and traceable. Balances reflected in the financial statements must reconcile with supporting schedules and working papers. Unexplained gaps typically lead to additional scrutiny.

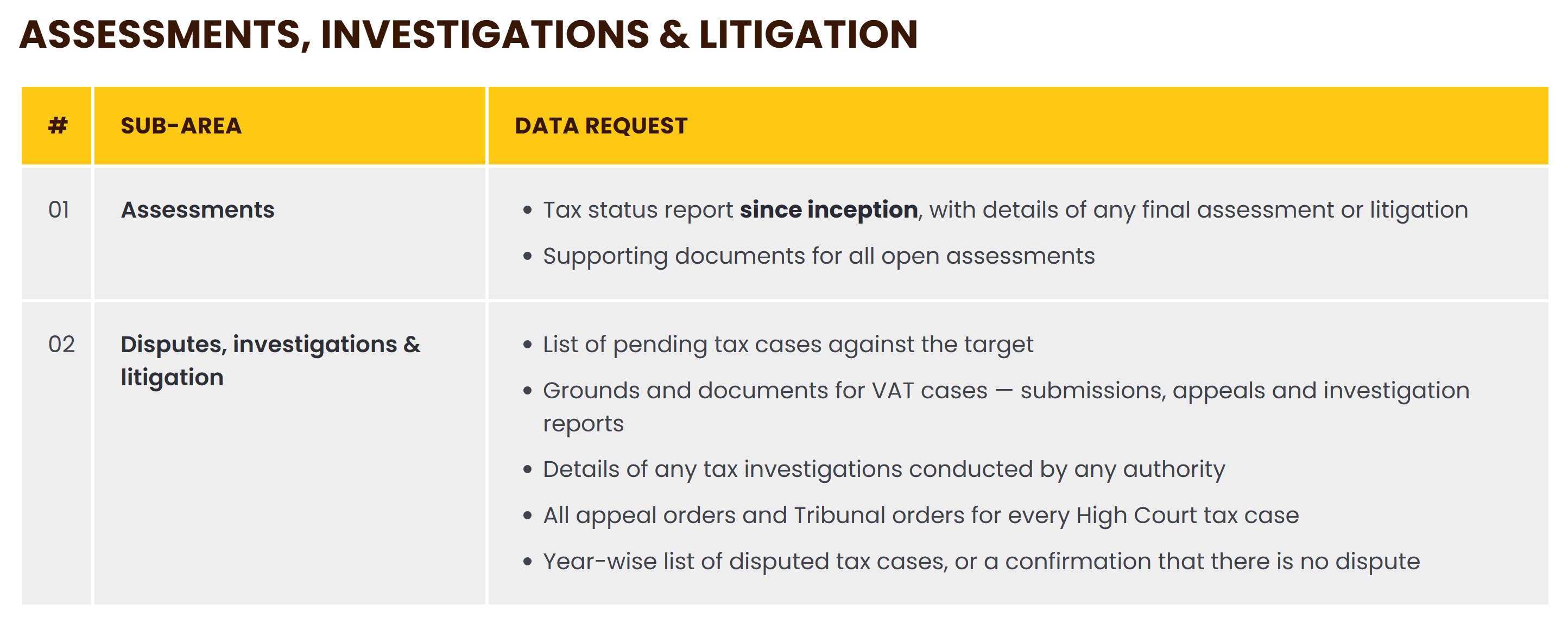

Segment 3: Assessments, Investigations & Litigation

Here, the focus moves from compliance to exposure. Investors review tax status reports since inception, documentation for open assessments, lists of pending cases, investigation reports, and appeal or tribunal orders. A year-wise summary of disputed tax cases is typically requested, or a formal confirmation that no disputes exist.

Tax disputes are common. What matters is transparency. Investors want to understand the nature of each issue, the financial exposure involved, the current stage of proceedings, and whether any provision has been recorded. Clear disclosure reduces perceived risk.

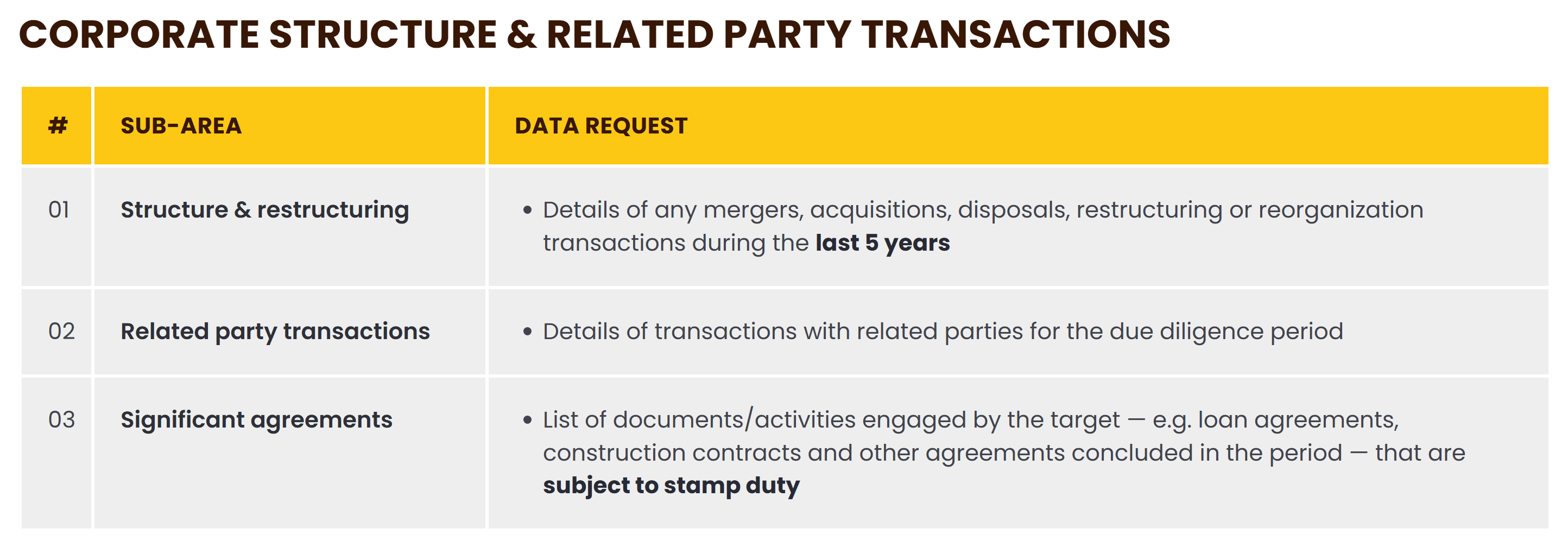

Segment 4: Corporate Structure & Related Party Transactions

Tax diligence also intersects with governance. Investors review any mergers, acquisitions, disposals, or restructuring events that occurred during the review period. Related party transactions are examined to assess documentation quality, commercial rationale, and tax implications. Significant agreements, such as loan contracts or financing arrangements, are also reviewed to evaluate withholding treatment and tax impact.

Poor documentation around related parties or restructuring creates governance concerns that can affect valuation discussions.

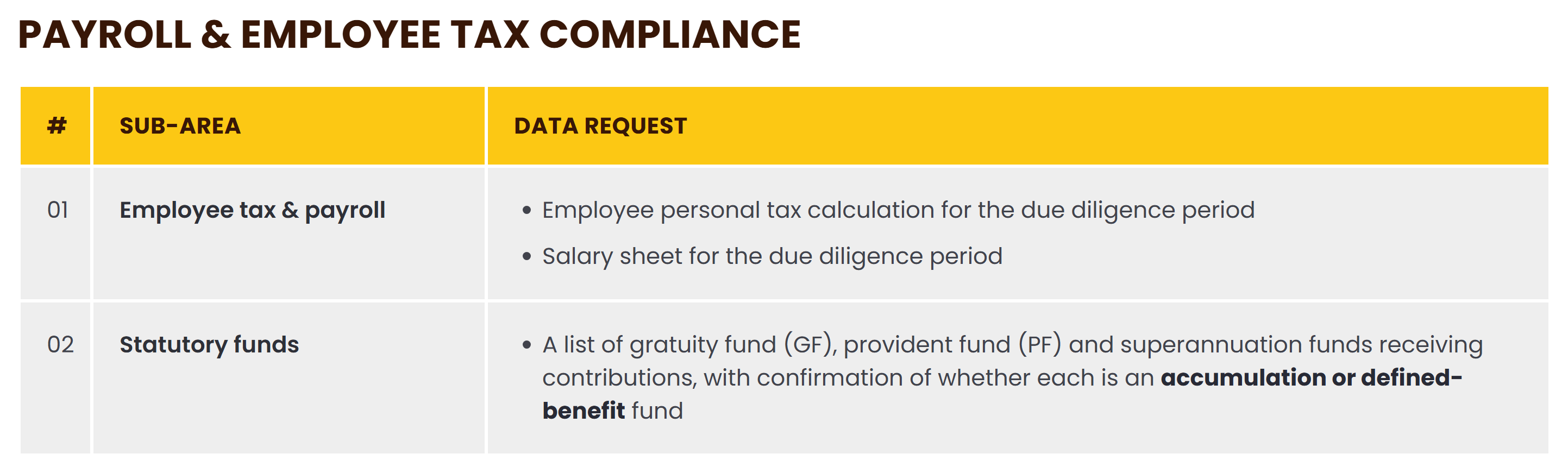

Segment 5: Payroll & Employee Tax Compliance

Payroll is one of the most sensitive tax areas. Investors review employee personal tax calculations, salary sheets for the relevant financial years, and details of contributions to provident fund, gratuity fund, superannuation, or similar statutory schemes.

This segment assesses whether payroll taxes were calculated correctly, withheld appropriately, and deposited on time. Non-compliance here creates direct statutory exposure and potential reputational risk.

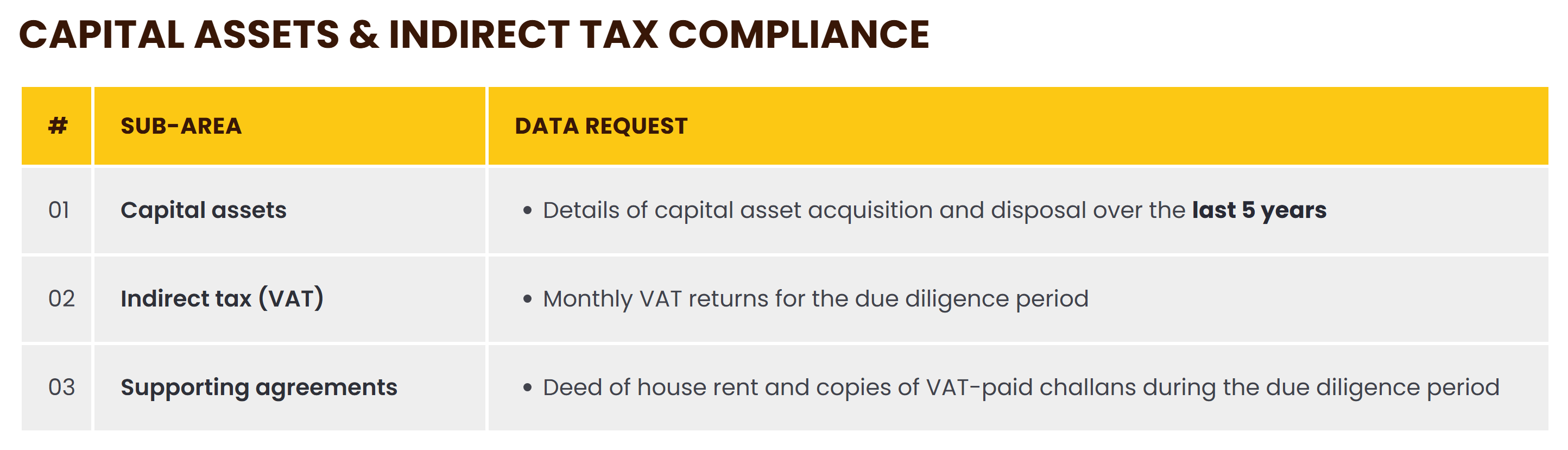

Segment 6: Capital Assets & Indirect Tax Compliance

This final segment connects operational activity to tax reporting. Investors examine capital asset acquisition and disposal history, monthly VAT returns for the due diligence period, VAT payment challans, and supporting agreements such as rent deeds, where applicable.

The objective is to confirm that asset records align with tax treatment and that VAT filings reconcile with sales and purchase registers. Most indirect tax issues arise from reconciliation gaps rather than intent. When operational records and tax filings are aligned, this section moves quickly.

Wrapping Up

Tax due diligence is about whether filings reconcile, exposures are clearly disclosed, and documentation is organized. When tax records are structured and traceable, diligence moves faster.

In Part 1, the financial story was prepared. In this part, the compliance side was addressed. In the final part, Legal Due Diligence will be covered.

Related Articles

View All

.jpg)

.jpg)

.png)

.jpg)

.jpg)

.jpeg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpeg)