What Investors Actually Check in Legal Due Diligence

Insight

Subscribe to our

Newsletter

Newsletter

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Shoumik Shahriar is a Senior Business Consultant and Project Manager at LightCastle Partners, a management consulting firm based in Bangladesh.

Legal due diligence is where most startups are least prepared, not because the issues are complex, but because the problems are almost always fixable documentation gaps that no one got around to fixing.

This is the third and final part of a three-part series on due diligence preparation for fundraising. Part one covered financial due diligence and part two covered tax due diligence.

Legal due diligence (LDD) is the investor's way of answering three questions:

- Is this company properly constituted and legally clean?

- Are the contracts this company depends on enforceable and risk-free?

- Does this company own what it claims to own?

This article walks through a practical LDD preparation structure, based on what investors and their legal counsel actually review.

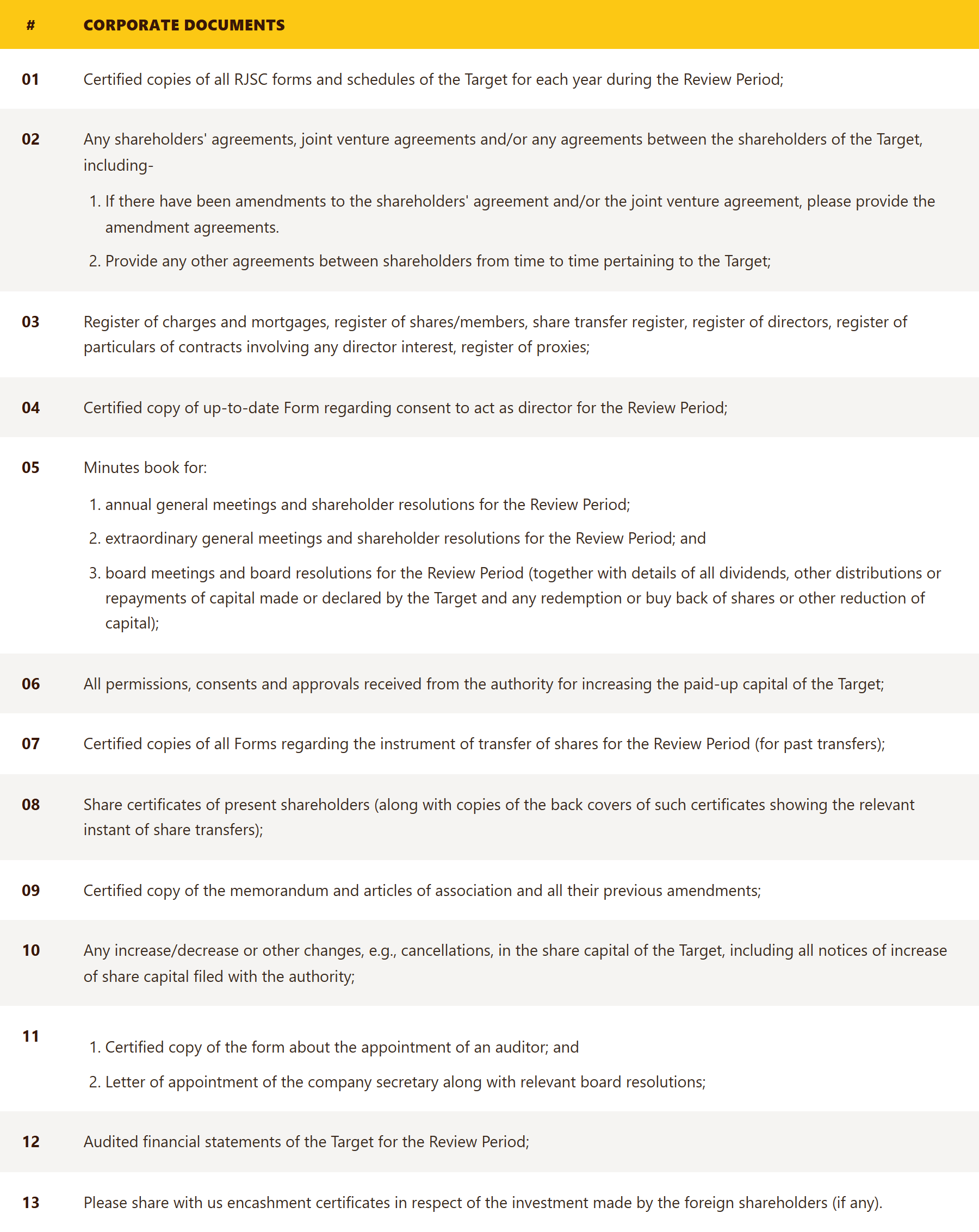

Segment 1: Corporate Documents

This is where LDD begins. Before investors look at contracts or liabilities, they need to confirm that the company exists in the form it claims to. Certified corporate filings confirm the company's registered status over the review period. The memorandum and articles of association define what the company is legally permitted to do. Minutes books for board meetings, AGMs, and EGMs show how governance decisions were made and documented. Share certificates, transfer registers, and allotment forms establish the full ownership history. Regulatory approvals for capital increases confirm regulatory compliance at every stage of the equity issuance process.

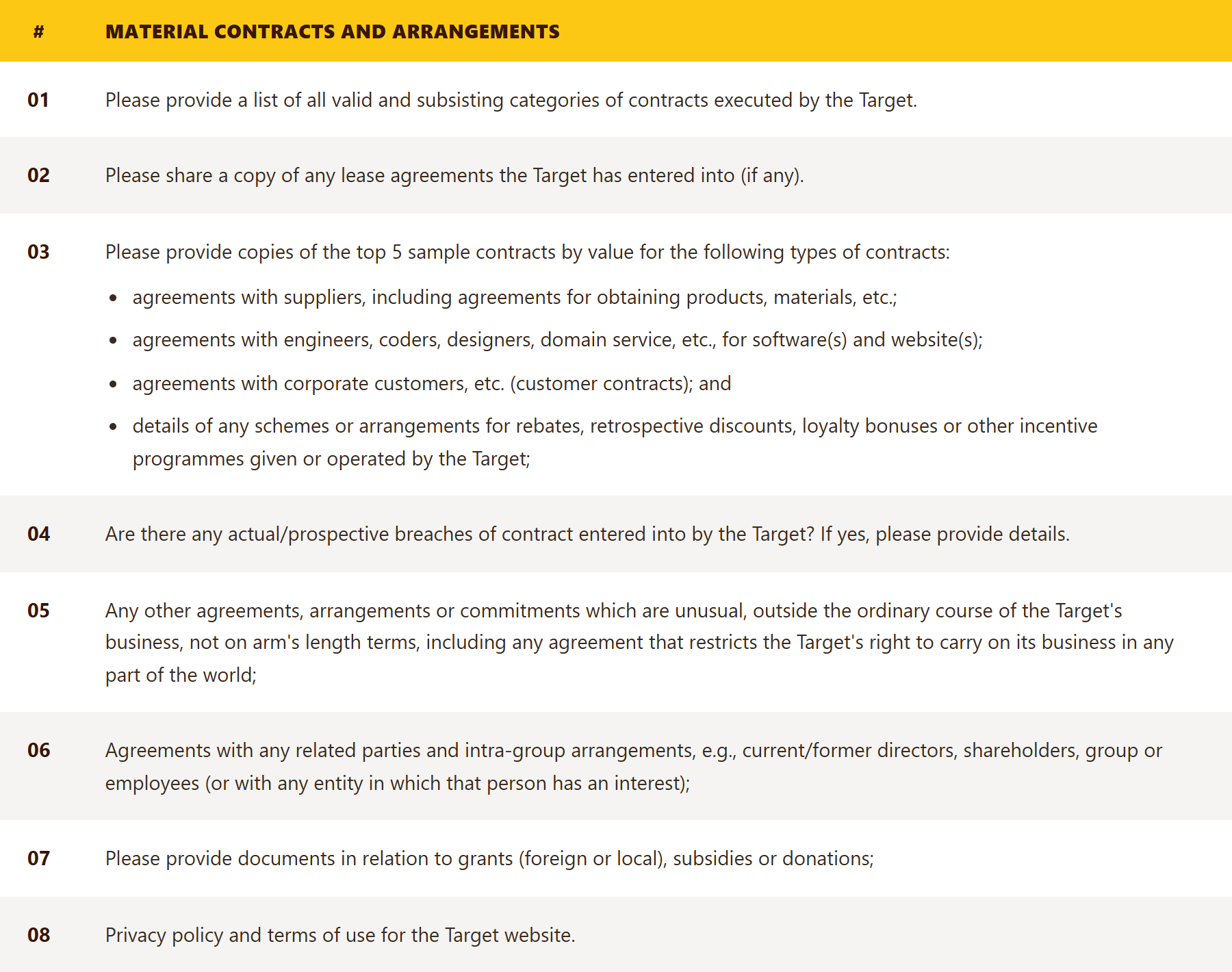

Segment 2: Material Contracts and Arrangements

This segment is where investors test whether key contracts are real, enforceable, and risk-free. A full list of valid and subsisting contracts shows how operationally dependent the company is on external relationships. Top supplier and customer contracts reveal concentration risk and the quality of commercial terms. Lease agreements define property obligations and long-term fixed costs. Related-party agreements expose transactions between the company and its directors, shareholders, or group entities that may not be at arm's length. Breach disclosures and unusual arrangements outside ordinary business are reviewed for exposure and contingent liability. Privacy policies and website terms of use confirm consumer-facing regulatory compliance. Investors read contracts looking for exit clauses, change-of-control provisions, and termination triggers.

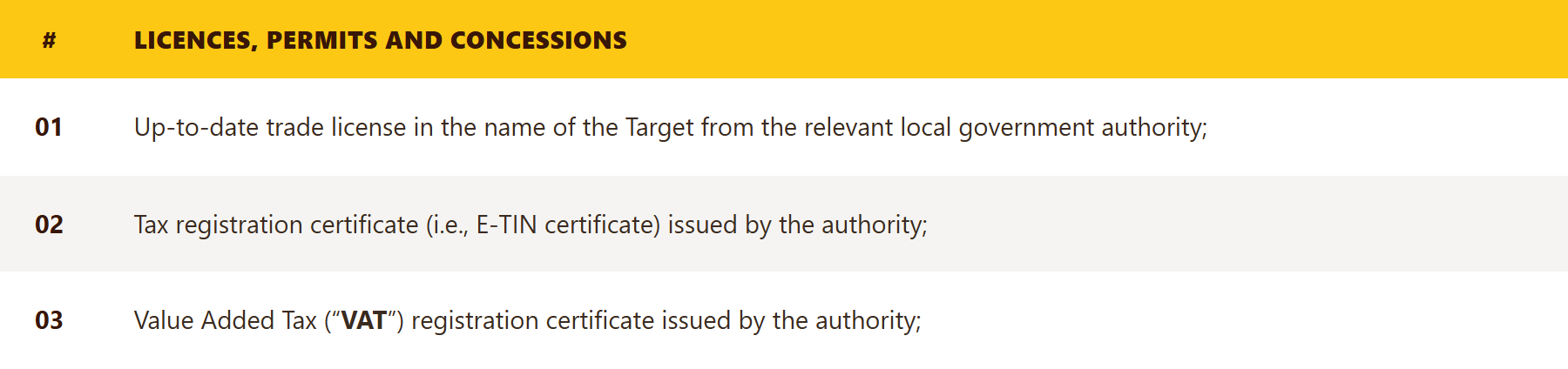

Segment 3: Licences, Permits, and Regulatory Compliance

A company may be operationally successful and still legally fragile if it is operating without the right permissions. An up-to-date trade licence confirms the company has the right to operate in its jurisdiction. The e-TIN certificate establishes tax registration and compliance. The VAT registration certificate confirms the company is correctly registered for indirect tax purposes. This segment is short, but the consequences of gaps here are disproportionately large. An expired trade licence or a missing VAT registration is a regulatory liability that an investor must either fix or price into the deal.

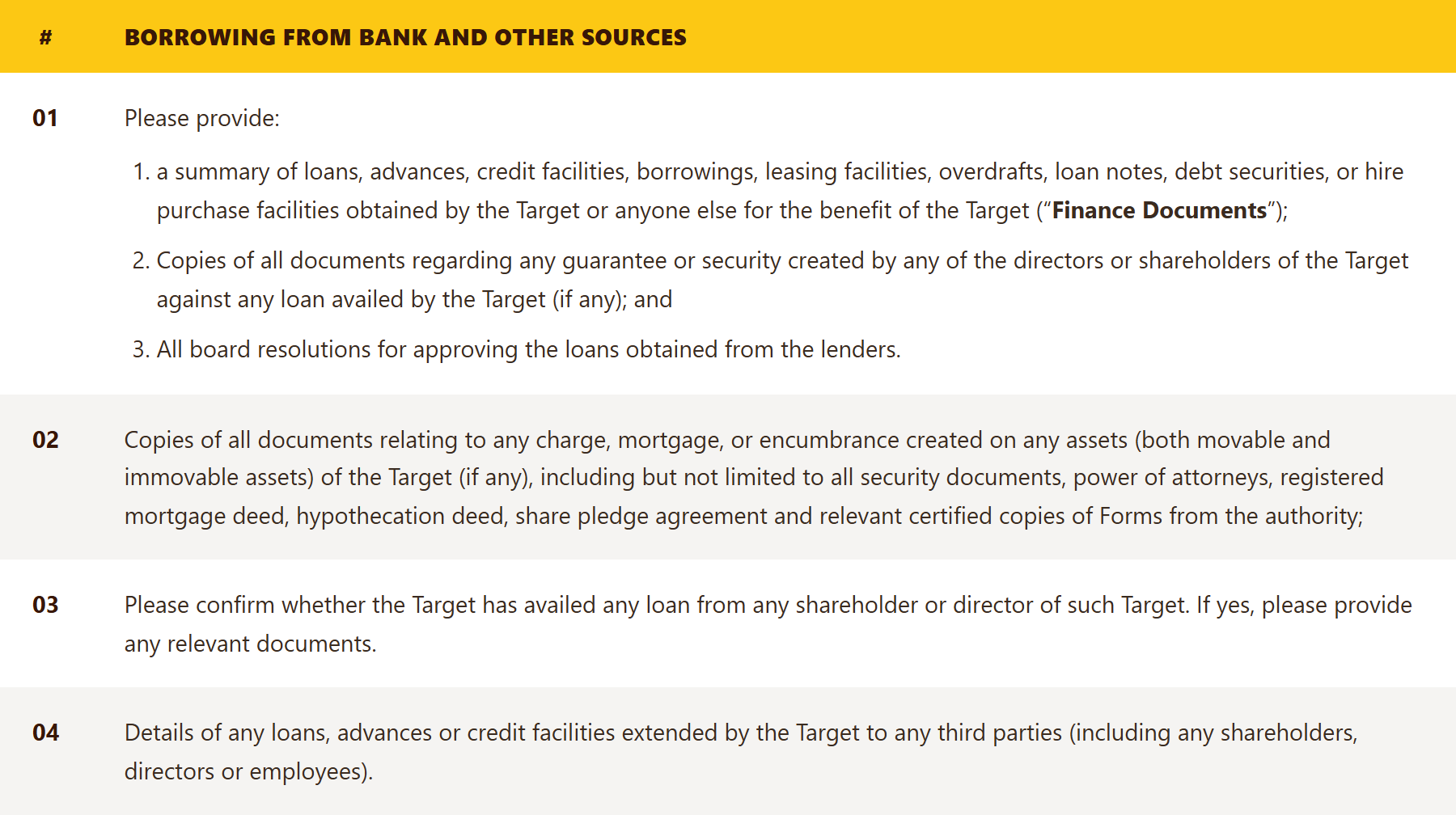

Segment 4: Borrowings and Financial Obligations

Investors use this segment to map every financial obligation the company carries. A summary of all loans, credit facilities, overdrafts, leasing arrangements, and hire purchase facilities shows the full debt picture. Charges, mortgages, and encumbrances registered on moveable and immovable assets reveal what has been pledged as security. Board resolutions for loan approvals show that borrowing decisions were properly authorised. Guarantees provided by directors or shareholders for company debt create personal exposure that investors need to understand. Loans extended by the company to third parties, including employees, shareholders, or directors, are reviewed for related-party risk.

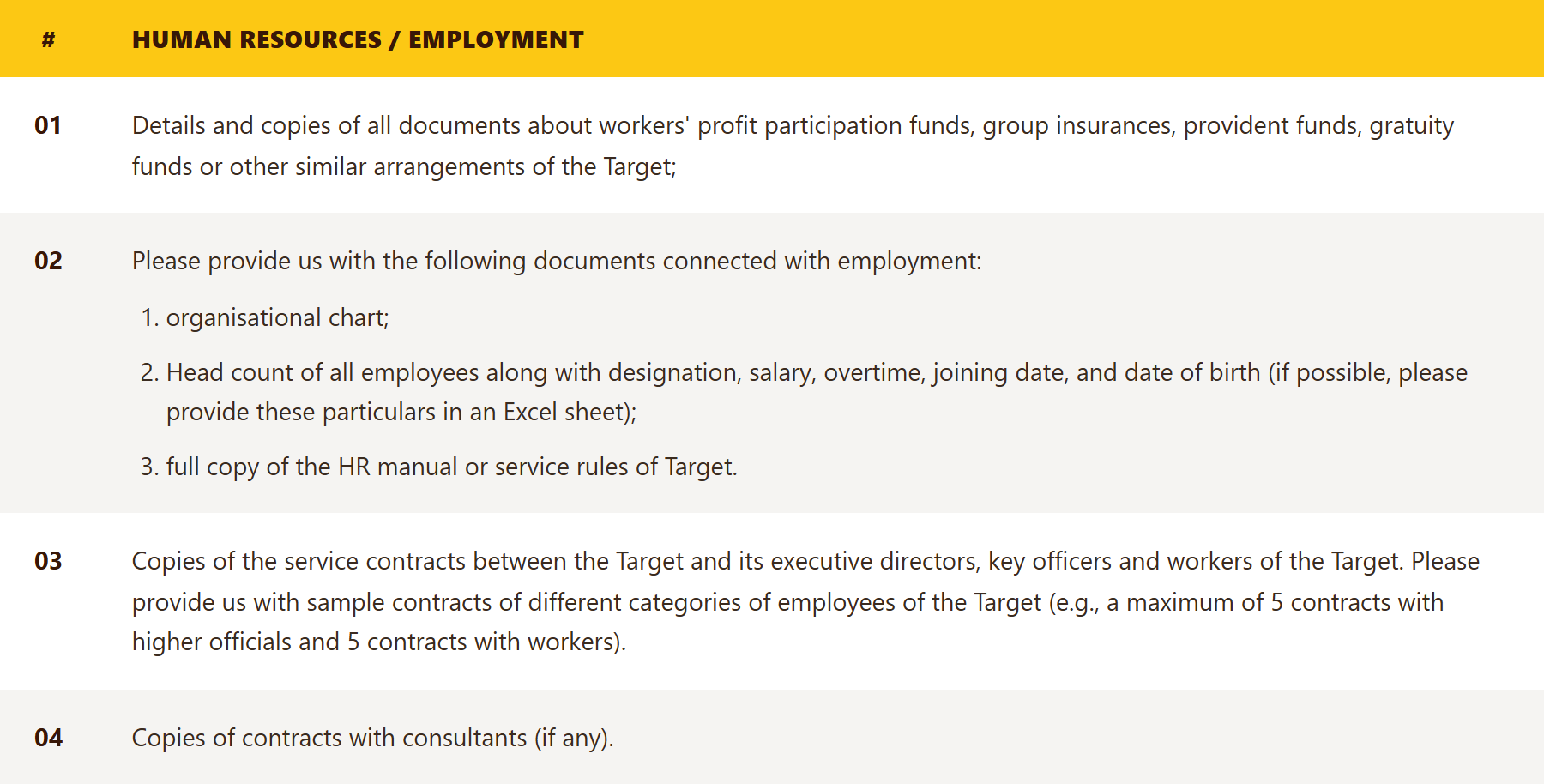

Segment 5: Human Resources and Employment

People are usually a startup's highest cost and its most complex legal obligation. This segment tests whether that obligation is managed properly. An organisational chart and full headcount data give investors a complete picture of the employment base. Service contracts for executive directors, key officers, and workers confirm that employment terms are documented and legally compliant. The HR manual and service rules show whether policies governing leave, conduct, discipline, and termination are formalised. Documentation for provident funds, gratuity funds, group insurance, and workers' profit participation funds confirms that statutory benefit obligations are met. Consultant contracts are reviewed separately to assess whether contractor arrangements carry hidden employment classification risk.

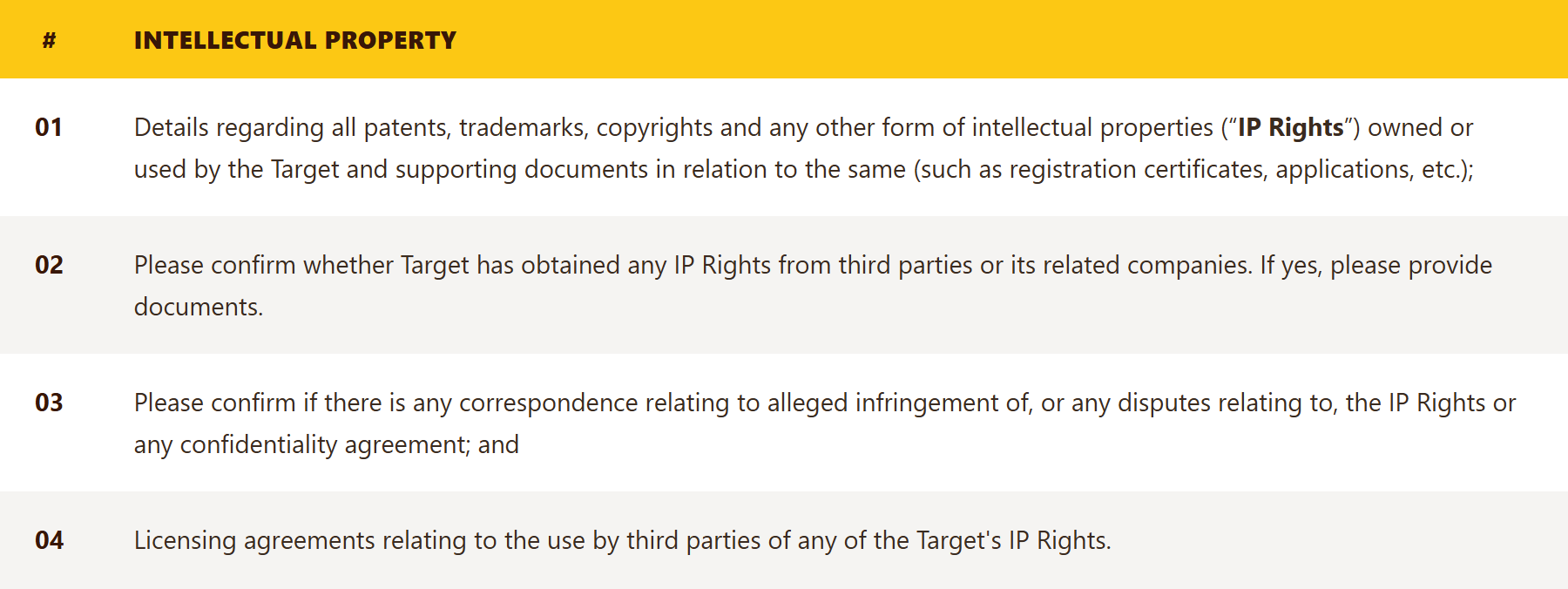

Segment 6: Intellectual Property and Litigation

For most startups, intellectual property is the asset. This segment tests whether the company actually owns what drives its value, and whether that ownership is under threat. Details of all patents, trademarks, copyrights, and other IP rights, with supporting registration certificates, establish what is legally protected. IP sourced from third parties or related companies is reviewed for licence terms, exclusivity, and dependency risk. Any correspondence about alleged infringement, disputes, or confidentiality breaches reveals whether the IP ownership is contested. Licensing agreements under which the company grants others the right to use its IP are checked for value leakage and control provisions. Pending or threatened litigation, regulatory inquiries, arbitral proceedings, or statutory investigations are disclosed in full, with the latest status of each matter.

Wrapping Up

Legal due diligence is not about looking perfect. It is about being organised, transparent, and prepared. Most legal issues that delay fundraising rounds are not fundamental problems. They are documentation gaps, expired registrations, or informal contracts. These are fixable yet time-consuming matters. If you can walk a lawyer through your data room without hesitation, you are already ahead of most founders.

Related Articles

View All

.jpg)

.png)

.jpg)

.jpg)

.jpeg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpeg)